Prospective homebuyers are hitting the pavement as rates drop to their lowest level since mid-December. But that hasn’t yet translated to sales.

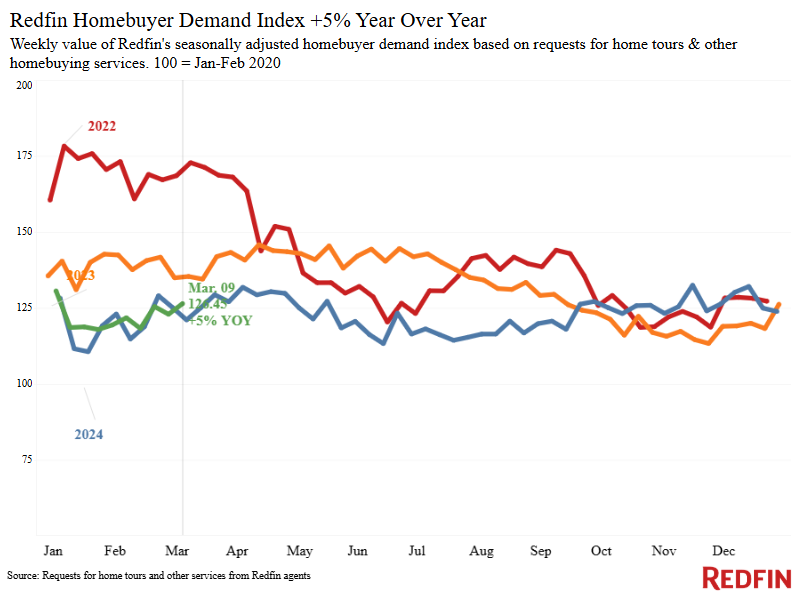

More house hunters are touring homes as mortgage rates decline. Mortgage-purchase applications rose 7% this week to their highest level since the start of February as weekly average mortgage rates dipped to their lowest level since mid-December. Google searches of “homes for sale” are up 10% year over year to their highest level since July, and Redfin’s Homebuyer Demand Index–a seasonally adjusted measure of home tours and other buying services from Redfin agents–hit its highest level since the start of the year.

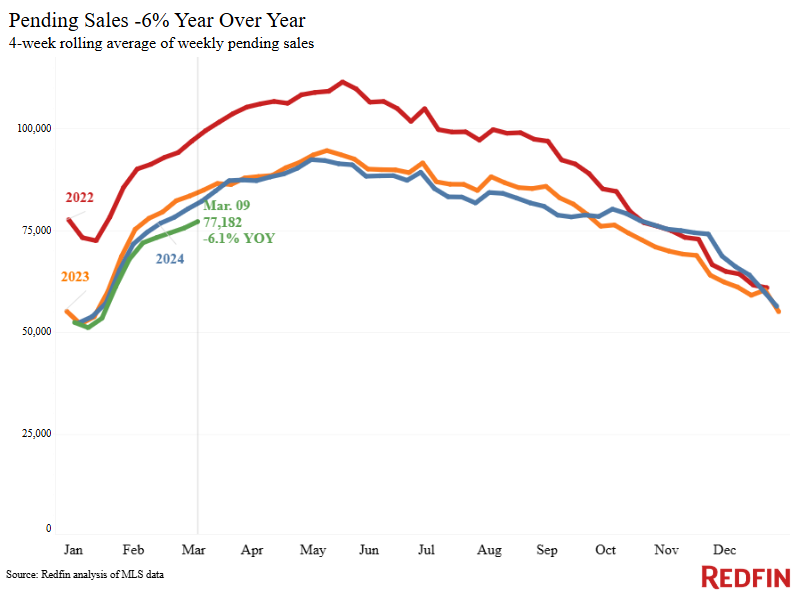

The uptick in house hunting hasn’t yet translated to an uptick in home sales. Pending home sales fell 6.1% year over year during the four weeks ending March 9, on par with declines over the last few months.

“Mortgage rates are coming down because the country’s economic outlook is getting stormier as investors worry about things like tariffs and a slightly weaker-than-expected job market,” said Redfin Economic Research Lead Chen Zhao. “Lower mortgage rates have brought some house hunters who were waiting for costs to come down off the sidelines. But they haven’t yet led to more sales because prospective buyers are still figuring out whether lower payments are enough to justify a home purchase in today’s uncertain economy. Many Americans are concerned about things like job security and a potential recession.”

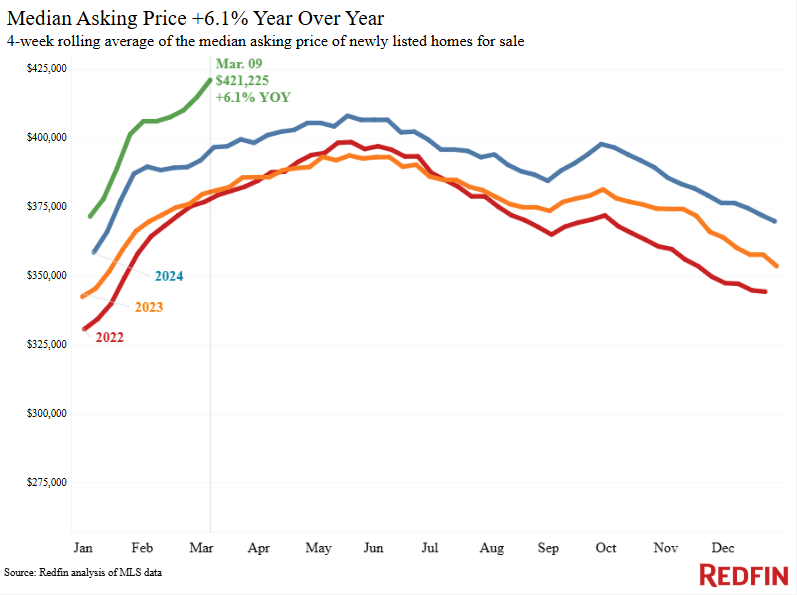

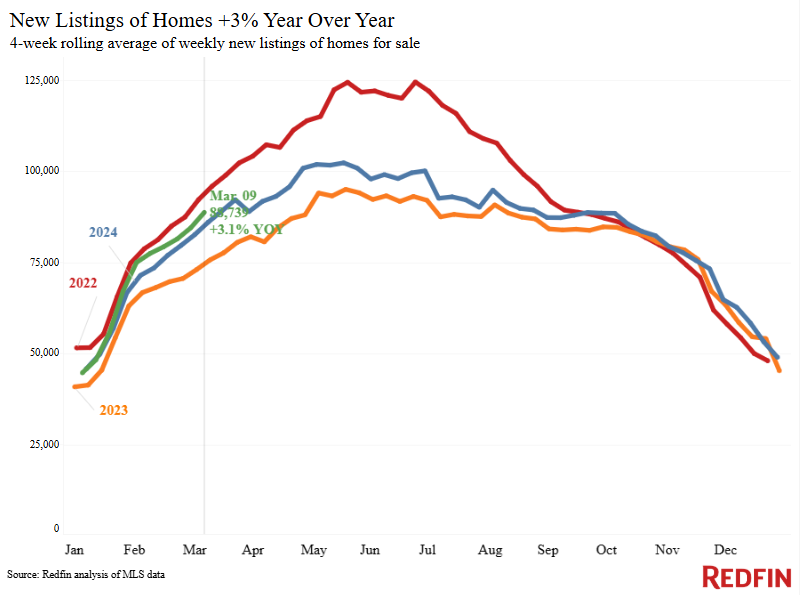

On the selling side, new listings of homes for sale are up 3.1% year over year, similar to the upticks we’ve seen over the last month. We expect listings to continue ticking up as we enter spring homebuying season, and homeowners notice increasing demand from buyers.

For Redfin economists’ takes on the housing market, please visit Redfin’s “From Our Economists” page.

Leading indicators

| Indicators of homebuying demand and activity | ||||

| Value (if applicable) | Recent change | Year-over-year change | Source | |

| Daily average 30-year fixed mortgage rate | 6.82% (March 12) | Up from 6.7% a week earlier, but still near lowest level since Dec. 6 | Down from 6.87% | Mortgage News Daily |

| Weekly average 30-year fixed mortgage rate | 6.63% (week ending March 6) | Lowest level since mid-December | Down from 6.88% | Freddie Mac |

| Mortgage-purchase applications (seasonally adjusted) | Up 7% from a week earlier (as of week ending March 7) | Up 4% | Mortgage Bankers Association | |

| Redfin Homebuyer Demand Index (seasonally adjusted) | Highest level since start of 2025 (as of week ending March 9) | Up 5% | Redfin Homebuyer Demand Index, a measure of tours and other homebuying services from Redfin agents | |

| Touring activity | Up 32% from the start of the year (as of March 10) | At this time last year, it was up 29% from the start of 2024 | ShowingTime, a home touring technology company | |

| Google searches for “home for sale” | Up 10% from a month earlier (as of March 10) | unchanged | Google Trends | |

Key housing-market data

| U.S. highlights: Four weeks ending March 9, 2025

Redfin’s national metrics include data from 400+ U.S. metro areas, and are based on homes listed and/or sold during the period. Weekly housing-market data goes back through 2015. Subject to revision. |

|||

| Four weeks ending March 9, 2025 | Year-over-year change | Notes | |

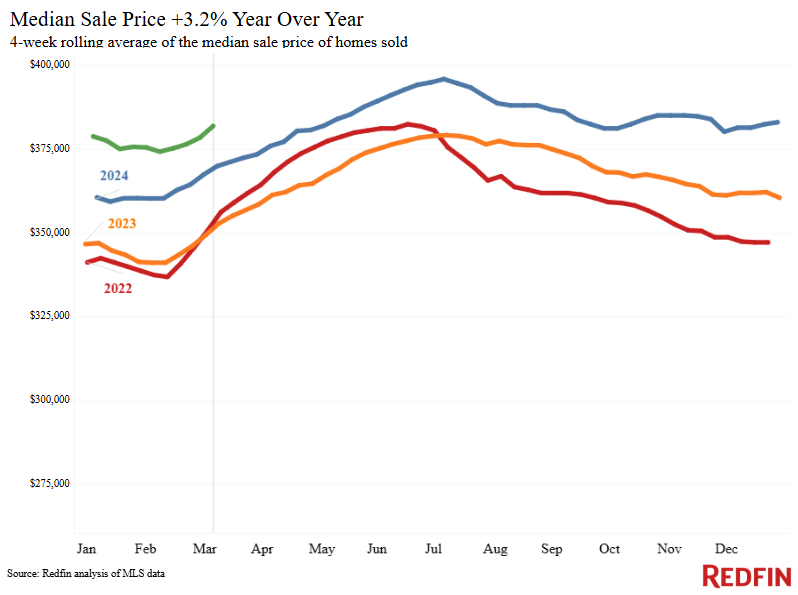

| Median sale price | $381,975 | 3.2% | |

| Median asking price | $421,225 | 6.1% | |

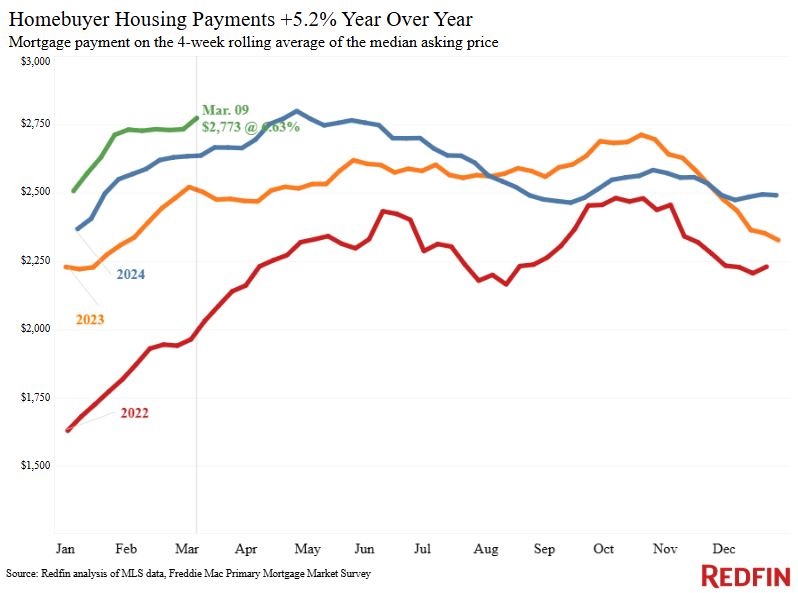

| Median monthly mortgage payment | $2,773 at a 6.63% mortgage rate | 5.2% | |

| Pending sales | 77,182 | -6.1% | |

| New listings | 88,739 | 3.1% | |

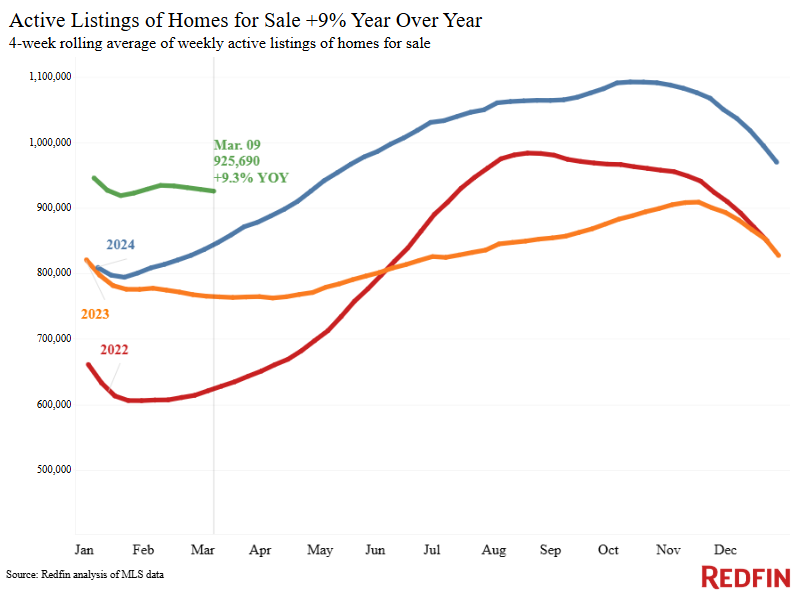

| Active listings | 925,690 | 9.3% | Smallest increase in over a year |

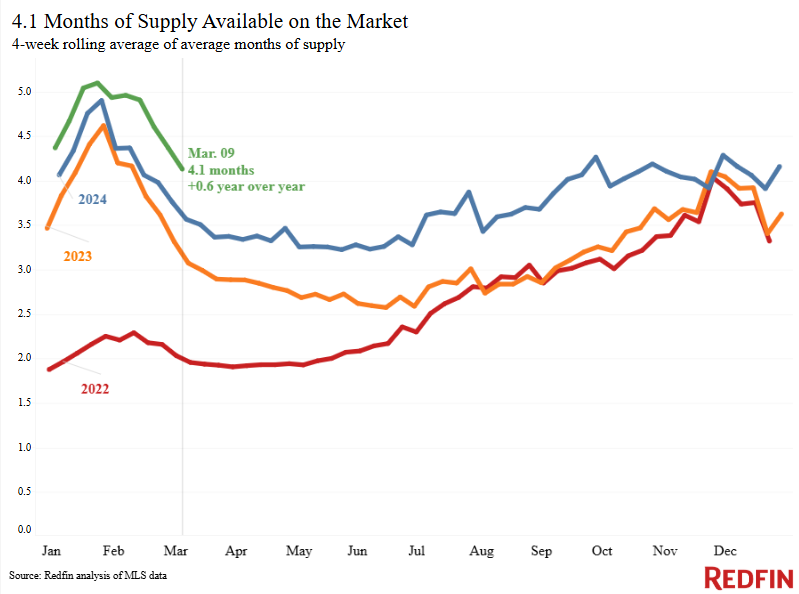

| Months of supply | 4.1 (lowest level of the year) | +0.6 pts. | 4 to 5 months of supply is considered balanced, with a lower number indicating seller’s market conditions |

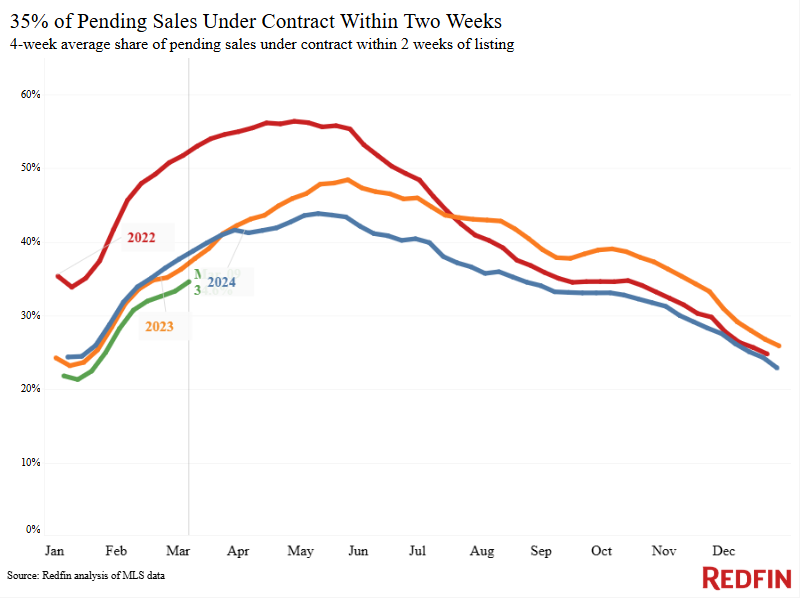

| Share of homes off market in two weeks | 34.6% | Down from 39% | |

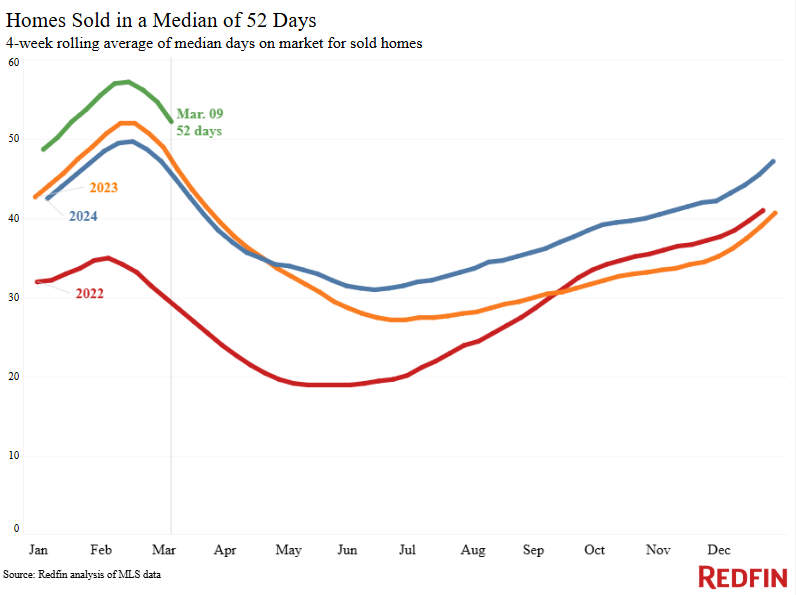

| Median days on market | 52 | +7 days | |

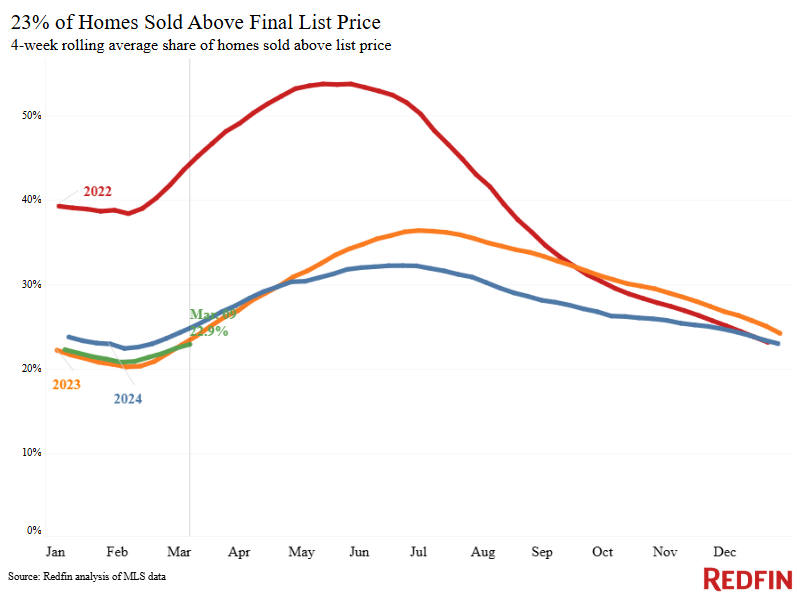

| Share of homes sold above list price | 22.9% | Down from 25% | |

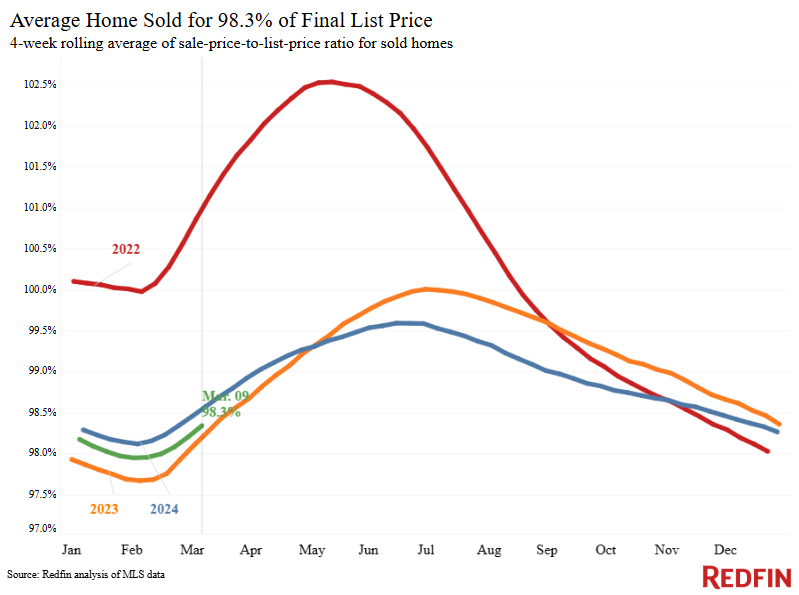

| Average sale-to-list price ratio | 98.3% | Down from 98.6% | |

|

Metro-level highlights: Four weeks ending March 9, 2025 Redfin’s metro-level data includes the 50 most populous U.S. metros. Select metros may be excluded from time to time to ensure data accuracy. |

|||

|---|---|---|---|

| Metros with biggest year-over-year increases | Metros with biggest year-over-year decreases |

Notes |

|

| Median sale price | Milwaukee (15.7%)

Cleveland (13%) Anaheim, CA (11.7%) Nassau County, NY (11.5%) San Jose, CA (10.3%) |

Austin, TX (-3.9%)

Jacksonville, FL (-2.6%) Tampa, FL (-2%) Atlanta (-1%) San Antonio (-0.8%) |

Declined in 5 metros |

| Pending sales | Los Angeles (3.3%)

Anaheim, CA (3.1%) Sacramento, CA (1%) |

Fort Lauderdale, FL (-16.6%)

Warren, MI (-16.1%) Houston (-15.6%) Atlanta (-14.8%) Detroit (-14.7%) |

Increased in 4 metros |

| New listings | San Jose, CA (35.7%)

Sacramento, CA (27.3%) Oakland, CA (25/2%) Phoenix (24%) Los Angeles (17.7%) |

Detroit (-18.3%)

Warren, MI (-13.1%) Austin, TX (-9.9%) Fort Worth, TX (-7.1%) Milwaukee (-6.6%) |

Increased in roughly half the metros |

Refer to our metrics definition page for explanations of all the metrics used in this report.

Written by: Dana Anderson