Homebuying activity picked up in November as election uncertainty dissipated and buyers grew more accustomed to elevated mortgage rates. Existing home sales for the full year will likely be in line with 2023 levels, but we expect activity to tick up in 2025.

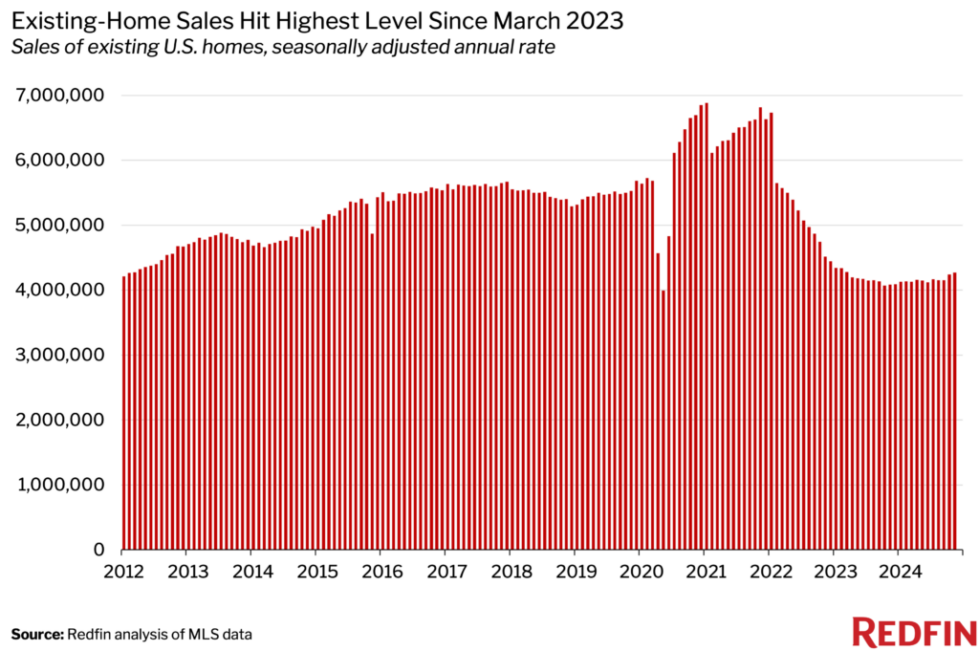

Existing home sales rose 0.7% month over month in November to a seasonally adjusted annual rate of 4,269,851—the highest level since March 2023. They jumped 4.5% year over year—the largest annual increase since July 2021.

A seasonally adjusted annual rate is not a measurement of actual total sales for the year, but rather, the pace of sales at a given time. A seasonally adjusted annual rate of 4,269,851 in November means that existing home sales would end the year at that level if homes were sold at the November pace for each month of 2024. Redfin’s measure of existing home sales has them coming in at around 4.1 million for the full year of 2024.

“Homebuying activity picked up steam in recent months as election uncertainty dissipated and house hunters realized that waiting probably isn’t going to get them a significantly lower mortgage rate anytime soon,” said Redfin Senior Economist Elijah de la Campa. “Since 2024 was a slow year for housing, existing home sales for the full year will still likely come in roughly the same as 2023, which was the weakest showing for sales since 1995. But we expect sales to tick up in 2025.”

The average interest rate on a 30-year mortgage rose to 6.81% last month, the highest level since July, but that’s still below the 7.44% level of November 2023. Mortgage rates hit the highest level in over two decades last fall, putting a damper on sales—another reason sales this past month posted a sizable year-over-year gain.

Overall home sales, including both existing and new homes, climbed 2.2% month over month in November to the highest level in over two years on a seasonally adjusted basis. They were up 7% year over year, the biggest annual increase since June 2021.

Pending sales also inched up, rising 0.4% month over month to the highest level since February 2023 on a seasonally adjusted basis, and climbing 5.7% year over year.

“The market was stagnant in the months leading up to the election, but within 48 hours of the results being announced, I was getting more home-tour requests,” said Rafael Corrales, a Redfin Premier real estate agent in Miami. “We definitely saw an uptick in demand on the buyside, but less so with listings.”

November 2024 Housing Market Highlights: United States

| November 2024 | Month-over-month change | Year-over-year change | |

|---|---|---|---|

| Median sale price | $430,107 | -0.9% | 5.4% |

| Existing home sales, seasonally adjusted annual rate | 4,269,851 | 0.7% | 4.5% |

| Pending home sales, seasonally adjusted | 495,299 | 0.4% | 5.7% |

| Homes sold, seasonally adjusted | 441,032 | 2.2% | 7.0% |

| New listings, seasonally adjusted | 525,178 | -1.6% | -4.8% |

| Total homes for sale, seasonally adjusted (active listings) | 1,736,884 | 0.5% | 12.1% |

| Months of supply | 3.1 | 0.1 | 0.1 |

| Median days on market | 43 | 2 | 6 |

| Share of homes sold above final list price | 26.5% | -1.3 ppts | -2.3 ppts |

| Average sale-to-final-list-price ratio | 98.8% | -0.2 ppts | -0.2 ppts |

| 6.81% | 0.38 ppts |

-0.63 ppts |

Note: Data is subject to revision

Home Prices Posted Biggest Gain in Seven Months as Supply Remained Constrained

The median home sale price increased 5.4% year over year to $430,107 in November, the biggest annual gain since April.

Prices continue to rise because there’s still a shortage of homes for sale. New listings fell 1.6% month over month on a seasonally adjusted basis and dropped 4.8% year over year.

While new listings slowed in November, active listings—a measure of all homes on the market—continued to rise. Active listings climbed 0.5% month over month to the highest level on a seasonally adjusted basis since July 2020, and increased 12.1% year over year. One reason active listings are rising is that some homes are taking a long time to sell, causing stale supply to pile up. The typical home that went under contract in November was on the market for 43 days—the slowest November pace since 2019.

While active listings rose last month, they were still 18.2% below pre-pandemic (November 2019) levels. New listings were 13.8% below pre-pandemic levels.

Metro-Level Highlights: November 2024

The bullets below are based on a list of the 50 most populous U.S. metropolitan areas. Some metros may be removed from time to time to ensure data accuracy. A full metro-level data table can be found in the “download” tab of the dashboard in the monthly section of the Redfin Data Center. Refer to our metrics definition page for explanations of metrics used in this report. Metro-level data is not seasonally adjusted. All changes below represent year-over-year changes.

- Prices: Median sale prices rose most from a year earlier in Philadelphia (19.2%), Newark, NJ (14.4%) and St. Louis (11.8%). They fell in just two metros: Tampa, FL (-1.3%) and Dallas (-0.6%).

- Pending sales: Pending sales rose most in Seattle (15.3%), Jacksonville, FL (14.9%) and Nashville (14.8%). They fell most in Miami (-12.5%), West Palm Beach, FL (-6.8%) and Fort Lauderdale, FL (-6%).

- Closed home sales: Home sales rose most in Portland, OR (27.6%), San Jose, CA (26.2%) and Seattle (19.5%). They fell most in West Palm Beach (-18.3%), Fort Lauderdale (-14.2%) and Philadelphia (-10.6%).

- New listings: New listings rose most in San Francisco (8.5%), Washington, D.C. (5.3%) and Fort Lauderdale (4.5%). They fell most in Austin, TX (-24.5%), Portland (-20.3%) and Atlanta (-18.5%).

- Active listings: Active listings rose most in Cincinnati (36.3%), Fort Lauderdale (34.3%) and San Diego (28.9%). They fell most in Newark (-2.5%), San Francisco (-1.8%) and Detroit (-1.6%).

- Sold above list price: In Newark, 64.8% of homes sold above their final list price, the highest share among the metros Redfin analyzed. Next came San Jose (58.6%) and Nassau County, NY (54.1%). The lowest shares were in West Palm Beach (6.7%), Fort Lauderdale (8.1%) and Miami (8.1%).

Written by: Lily Katz