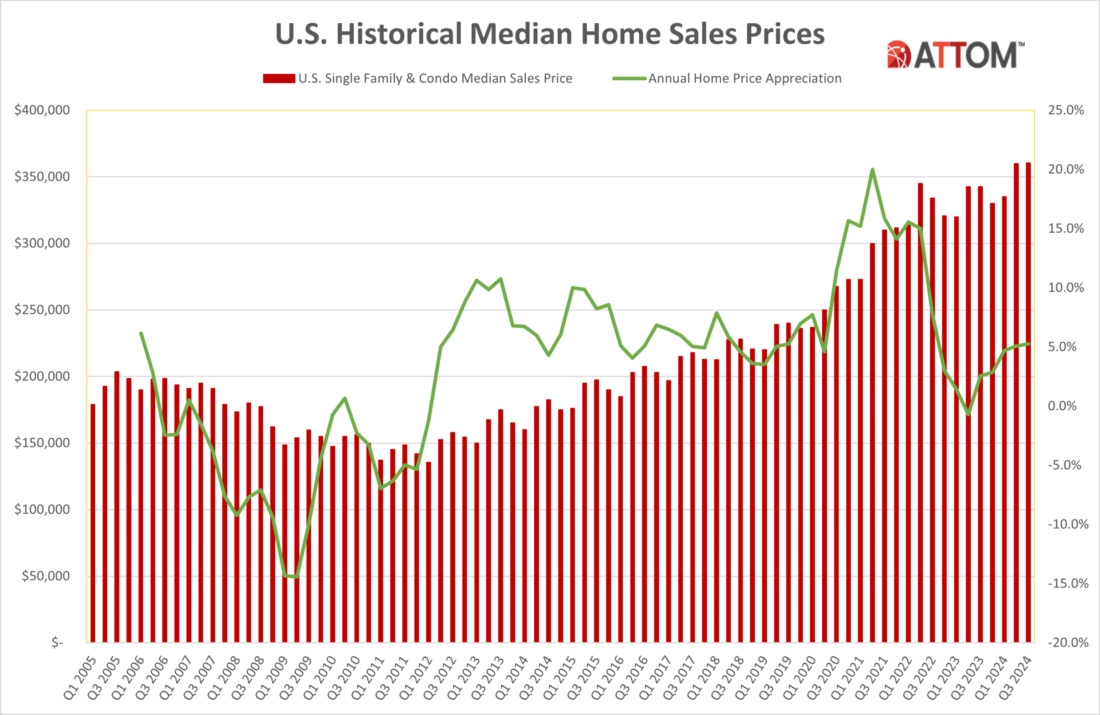

Key Insights on Foreclosures, Affordability, Home Prices, and Sales Trends Florida, the Sunshine State, presents a dynamic real estate market influenced by various factors, including economic cycles, migration patterns, and natural disasters. Using data from ATTOM, we explore key aspects such as foreclosures, affordability, home prices, and recent sales trends. In Q4 2024, the home affordability index varied significantly across different counties in Florida. For instance, Miami-Dade County had a median sales price of $525,000 and an affordability index of 62, indicating higher home prices relative to local incomes. Broward County, with a median sales price of $440,000, had an affordability index of 59, also reflecting affordability challenges. On the other hand, counties like Alachua and Bay offered relatively more affordable options. Alachua County had a median sales price of $303,000 and an index of 72, while Bay County’s median price was $365,000 with an index of 67. Foreclosure activity …