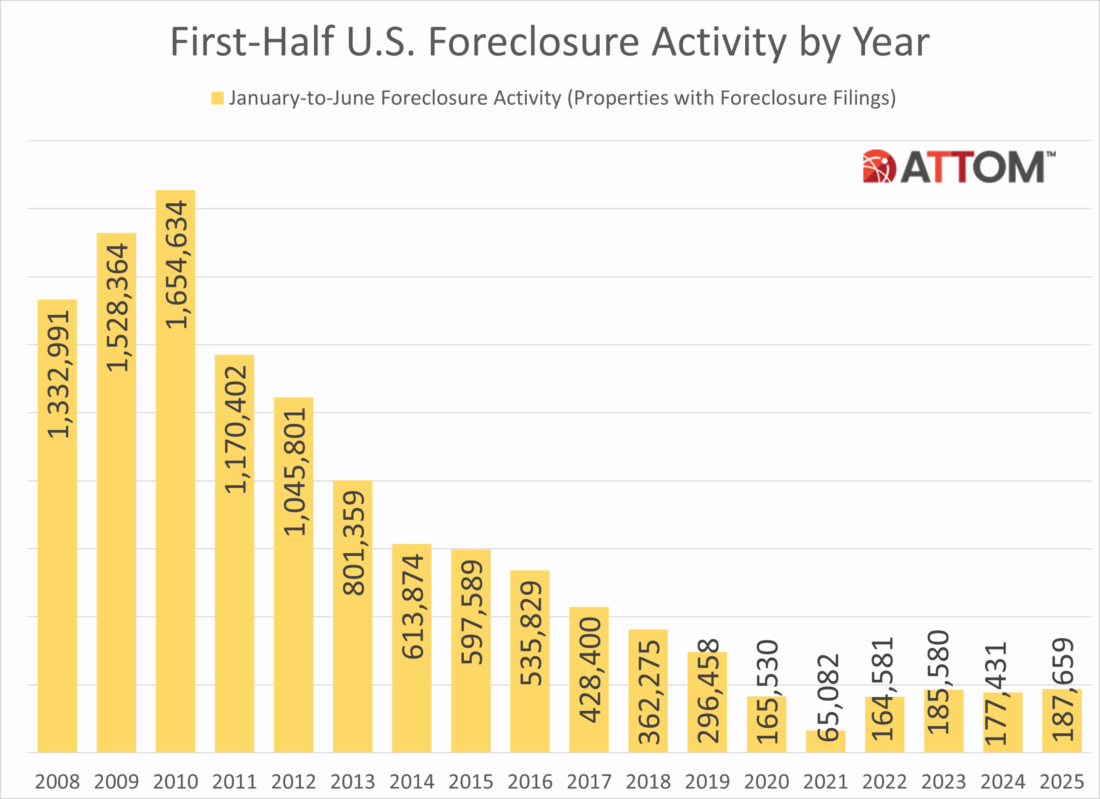

U.S. Foreclosure Starts increase 7 Percent in First Six Months of 2025; Average Days to Complete a Foreclosure Down Third Quarter in a Row; June and Q2 2025 Foreclosure Activity Post Annual Increase IRVINE, Calif. — July 17, 2025 — ATTOM, a leading curator of land, property data, and real estate analytics, today released its Mid-Year 2025 U.S. Foreclosure Market Report, which shows there were a total of 187,659 U.S. properties with foreclosure filings — default notices, scheduled auctions or bank repossessions — in the first six months of 2025. That figure is up 5.8 percent from the same time period a year ago and up 1.1 percent from the same time period two years ago. “Foreclosure activity continued its upward trend in the first half of 2025, with increases in both starts and completed foreclosures compared to last year,” said Rob Barber, CEO at ATTOM. “While the overall numbers …